Introduction

Gold is red hot again!

While I am writing this, COMEX gold is trading at almost $2,400 per troy ounce, up more than 40% from the 2022 lows, when gold was trading at $1,650.

TradingView (COMEX Gold)

Even Costco (COST) started selling gold bars last year, selling out within a few hours!

As reported by The Wall Street Journal:

Gold buyers, especially those on the younger side, say it is a hedge against catastrophe. Even people who aren’t building bunkers and predicting doomsday are increasingly preparing for worst-case scenarios.

[…] The warehouse retailer said it sold $100 million in gold bars in 2023. It later added silver coins to its inventory. Precious metal sales helped drive 18% year-over-year growth in e-commerce sales during its most recent quarter, which ended in February, Costco said.

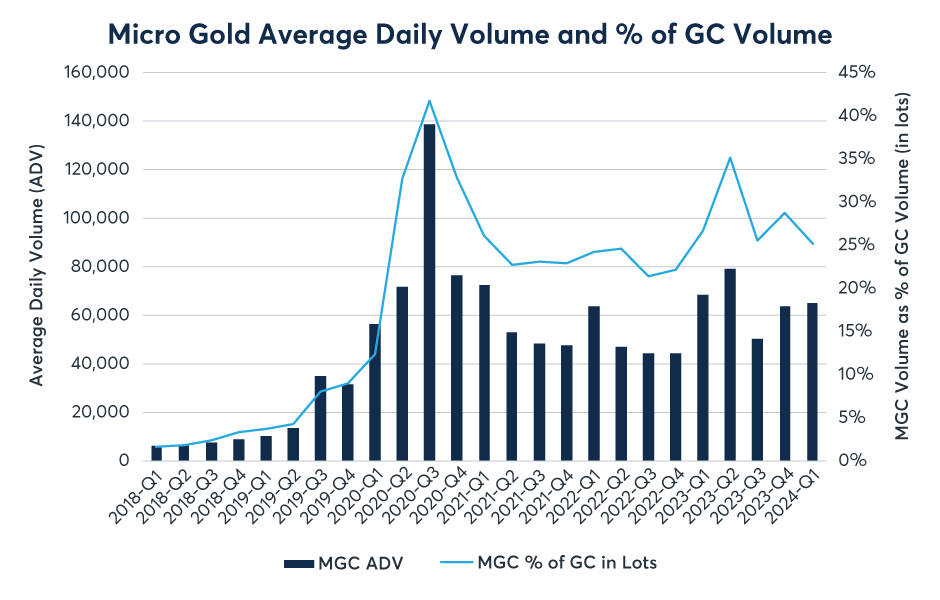

On the stock market, we find similar optimism, as average daily volumes of CME Group’s (CME) micro gold futures are substantially higher compared to levels seen in 4Q23 when gold was roughly $400 lower.

CME Group

With that said, there are many ways to invest in gold.

- Physical gold- This includes the aforementioned Costco gold, jewelry, or coins and bars from your local coin shop. I like this method a lot. However, due to safety reasons (I use my real name to discuss investments on the Internet), I do not buy physical gold or silver.

- ETFs & Futures- This method is easy, as investors can simply log into their brokerage account and invest in ETFs or buy futures.

- Miners- Gold miners produce gold. The higher the price of gold, the more money they make. However, as straightforward as that sounds, miners have, historically speaking, been horrible investments. They often deal with high operating costs and uncertainty, geopolitical risks, and other issues that have resulted in a horrible long-term return – especially compared to the price of gold.

But wait, there’s a fourth way.

On March 24, I wrote an article titled “Franco-Nevada: Forget Volatile Miners – This Is How To Win With Gold.”

That article was, as the title gives away, about Franco-Nevada (FNV), which is a gold streaming company.

In this article, I’ll cover its peer, Wheaton Precious Metals (NYSE:WPM), and explain why I consider it to be a fantastic precious metal play – superior to most miners.

So, without further ado, let’s get to it!

WPM’s Superior Business Model

Wheaton Precious Metals is the fourth-largest holding of the VanEck Gold Miners ETF (GDX). However, it is not a gold miner.

The company is a streamer.

What’s a streamer?

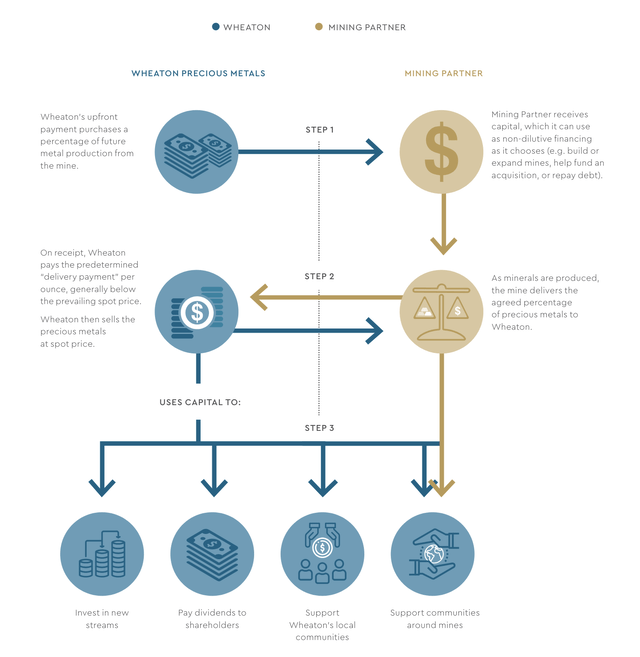

A streaming company benefits from rising gold and silver prices without producing any gold and silver itself. It’s a company that provides financing for mining projects.

As we can see below, the company provides upfront capital in exchange for a percentage of the future production of the mine, which it can buy below the spot price. That’s “streaming.”

Wheaton Precious Metals Corp.

It’s a genius high-margin business model that provides much-needed capital for expensive mining projects.

Miners need capital. Selling a percentage of future production at a discount is a sacrifice many are willing to make to protect their balance sheets and avoid shareholder dilution through equity funding.

Currently, the company’s portfolio includes 18 operating mines and 27 development projects.

The overview below shows some of its past investments, including the structure of its streams.

Wheaton Precious Metals Corp.

Looking at the 2024-2028 revenue mix below, we see the company expects 60% of its revenues to come from gold operations, followed by 36% from silver.

It’s the only major streaming company with near-100% precious metal exposure.

Moreover, most of its money is expected to be generated in rather safe jurisdictions, including Brazil, Mexico, Peru, Europe, Canada, and the United States.

Wheaton Precious Metals Corp.

Even better, more than 90% of its current production comes from assets that operate in the bottom half of the cost curve. It has 28 years of proven and probable production reserves.

That number rises to more than 60 years if we include measured/indicated and inferred reserves!

Wheaton Precious Metals Corp.

So far, so good.

However, it gets even better.

Because of large reserves and aggressive investments in growth, WPM is now reaping the benefits.

In the first quarter of 2024, Wheaton reported a production of 160,000 GEOs (gold equivalent ounces), which marks a 19% increase compared to the same quarter last year.

This increase was primarily driven by a 28% rise in gold production, mainly from the Salobo and Constancia mines in South America.

Wheaton Precious Metals Corp.

Sales volumes also saw a significant improvement, reaching 143,000 GEOs, a 31% year-over-year increase. The surge in sales was attributed to higher production levels and changes in ounces produced but not yet delivered.

On a full-year basis, the company is aiming to produce between 550,000 and 620,000 GEOs, with the potential to grow beyond 850,000 GEOs after 2029.

Wheaton Precious Metals Corp.

Through 2028 alone, the company aims to grow production by roughly 40%, with more than 80% of growth coming from re-risked assets that are either operating, in construction, and/or permitted.

Wheaton Precious Metals Corp.

This bodes well for its future, especially if it gets support from rising precious metal prices, as it has very low cash costs.

Using the latest data, the company expects total cash costs of $439 per troy ounce for gold production in the 2024-2028 period. For comparison, the world’s largest gold miner, Newmont (NEM), has an all-in-sustaining cost of roughly $1,300 per troy ounce.

Wheaton Precious Metals Corp.

The data above also shows the terrific operating leverage of streamers, with operating margins in the high 70% range.

In general, the company now benefits tremendously from past investments, as it has now recouped more than 100% of its initial upfront investments in current production.

Or, to put it differently, the company is now in a spot where it benefits from past investments and high growth expectations without the need for a lot of capital.

While I like a number of miners, it is very hard for the average miner to compete with this business model.

Wheaton Precious Metals Corp.

This bodes well for shareholders.

Consistent Dividend Growth & Valuation

Like most streamers, WPM has a fantastic balance sheet.

As we can see below, it has $306 million in net cash, which means more cash than gross debt. It also has $2 billion in undrawn credit.

Wheaton Precious Metals Corp.

With that said, the company is not a high-yield dividend stock, which may be the biggest “problem” that comes with owning any of the big streamers.

After hiking its dividend by 3.3% on March 14, it currently pays $0.155 per share per quarter. This translates to a yield of 1.1%, which is even below the S&P 500’s 1.3% yield.

However, there’s good news:

- Dividend growth is consistent.

- The company announced a more “progressive” dividend policy in its fourth quarter, as it now aims for a consistently higher payout ratio.

Prior to the new plan, it aimed for a 30% cash flow payout ratio. Now, it will pay out more to incorporate higher growth expectations.

And so when we looked at our growth profile coming forward, we realized that if that — with the current framework, we actually wouldn’t be raising the dividend even though we’re going to see some growth. And of course, current commodity prices would accelerate that. But we haven’t seen that growth for a couple of years. And we just felt that having been flat for a couple of years, it was time to add some growth. We’ve had substantive growth in our dividend, peer group-leading growth in our dividend over the last 5, 6 years, but it has actually been held flat for a couple of years, and we just thought it was time to give it a bump. – WPM 4Q23 Earnings Call

Wheaton Precious Metals Corp.

Since 2015, the company has grown its dividend by 14% annually.

Moreover, it has consistently beaten the gold miners GDX ETF, as the WPM/GDX ratio below shows. I compared it to the price of gold (red line) to emphasize the consistency of the stock’s outperformance.

TradingView (WPM/GDX, Gold)

The ratio below compares the WPM stock price to the price of gold. As we can see, when gold rises, WPM rises faster. When gold falls, WPM falls faster.

TradingView (WPM/Gold, Gold)

In other words, if you’re bullish on gold and not necessarily looking for physical gold, I believe WPM is a superior play.

This also applies to the valuation. Putting a valuation on a commodity-related stock is tough, as stock prices are often highly correlated to the underlying commodities – at least on a short to mid-term basis.

As we just saw, this also applies to WPM.

With regard to its valuation, investors have been buying eagerly, sending New York-listed shares up 11% on a year-to-date basis.

As a result, WPM currently trades at a blended P/E ratio of 45.8x. This may sound outrageously high. However, it’s not.

While the company’s long-term normalized P/E ratio is 33.5x, I’m applying a 40x multiple here. I did the same to Franco Nevada, as the past two decades saw a lot of gold price volatility and elevated CapEx requirements.

Now, things are looking much better. Payouts are rising, gold and silver prices are strong, and companies are slowly but steadily adjusting their dividend payout targets.

Moreover, during prior upswings in gold prices (like after the Great Financial Crisis), WPM traded consistently between 35-45x earnings.

FAST Graphs

Based on current earnings expectations ($1.35 in 2026E, according to the FactSet data in the chart above), the company is trading at its fair price.

The consensus analyst price target is $59, which is roughly 7% above the current price.

I am bullish because I expect gold and silver prices to remain in a (volatile) long-term uptrend, fueled by a situation where the Fed may be forced to cut rates if economic growth gets too weak.

While this is still a low-probability event, I believe that consistently elevated inflation could force the Fed to keep rates higher for longer, potentially causing an economic growth deterioration that eventually forces it to cut.

Historically speaking, almost all rate hike cycles have ended in a recession.

That said, the Fed does not even have to create a doomsday scenario, as gold usually starts rallying once the Fed stops hiking rates. As that has already happened (I think it is done with hiking rates), we know why the market has started to buy gold with both hands.

While I would not rule out a temporary correction after gold has become mainstream again, I think WPM has a very bright future, which is why I am currently assessing how I am going to incorporate gold/streamers in my long-term dividend growth portfolio.

Takeaway

In a surging gold market, Wheaton Precious Metals emerges as a standout investment with its unique streaming model.

Unlike traditional miners, WPM benefits from rising gold and silver prices without the operational risks.

With a diverse portfolio of assets and a progressive dividend policy, WPM offers consistent growth potential and solid shareholder returns.

Despite its seemingly high valuation, WPM’s long-term outlook remains bullish, especially in light of ongoing economic uncertainties and potential rate cuts.

For investors seeking exposure to precious metals, I believe WPM stands out as a superior play in the current market landscape.

Pros & Cons

Pros:

- Stable Investment: With its streaming model, WPM offers exposure to gold and silver prices without the operational risks of traditional mining companies.

- Consistent Dividend Growth: WPM has a progressive dividend policy, consistently increasing dividends by 14% annually since 2015.

- Strong Balance Sheet: With $306 million in net cash and $2 billion in undrawn credit, WPM maintains a robust financial position.

- Diversified Portfolio: WPM’s portfolio includes 18 operating mines and 27 development projects, providing diversification across different assets and jurisdictions.

Cons:

- Low Dividend Yield: Despite consistent growth, WPM’s dividend yield of 1.1% may not be appealing to investors seeking high income.

- Valuation Concerns: WPM’s current valuation, with a blended P/E ratio of 45.8x, may appear high to some investors, although it reflects the company’s growth prospects.

- Gold and Silver Price Volatility: Fluctuations in gold and silver prices can impact WPM’s revenues and stock performance, exposing investors to market volatility.

Read the full article here