There was a time when online retailers relied on precipitous growth to justify a lack of earnings. During the dotcom boom, it didn’t even matter if the company had no obvious path to profitability, growth was king.

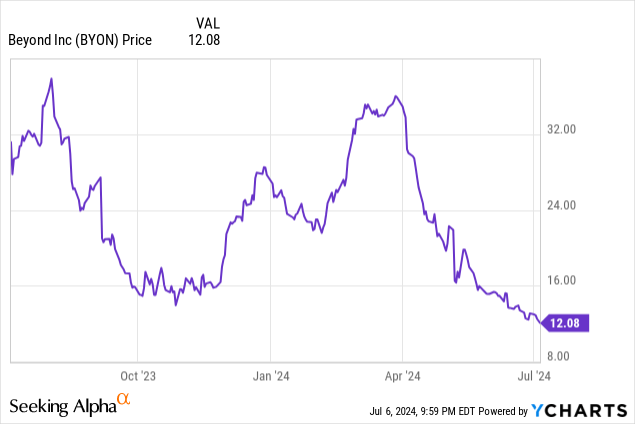

Today, we’ll be looking at online retailer Beyond (NYSE:BYON), formerly Overstock.com. The company has gone from one of the most recognizable names in online sales, to a badly punished company floating around its 52-week low.

The analysis of Beyond will focus on its possibility for a rebound, and whether it would be worth considering the company a bargain at these levels. This is, after all, the cheapest the company has been since 2020, and it is worth looking at where they are compared to where they were.

Understanding Beyond

As mentioned, Beyond has just undergone a name change. In November, the company was known as Overstock.com, and changed its name and ticker symbol.

Why change their name when Overstock was, for good or ill, such a recognizable name? The answer is Bed Bath & Beyond. In June 2023, Overstock acquired the brand and intellectual property assets of the bankrupt former retailer, spending around $25.6 million for their trouble.

Overstock.com was a big online seller of furniture and other home furnishings already, so acquiring the name and customer list of Bed Bath & Beyond made a sort of sense. Whether the very recognizable name has much cachet as it once did remains to be seen.

What is clear is that the combined company, Beyond, has become a source of high-quality home products at competitive prices, and is doing it to the tune of about $1.5 billion of sales per year.

Looking at Beyond’s Balance Sheet

|

Cash and Equivalents |

$256 million |

|

Total Current Assets |

$305 million |

|

Total Assets |

$577 million |

|

Total Current Liabilities |

$246 million |

|

Total Liabilities |

$289 million |

|

Total Shareholder Equity |

$288 million |

(source: most recent 10-Q from SEC)

If one was expecting Beyond to have the typical trappings of a dotcom retailer from 20+ years ago, they’d be very mistaken. The company has a lot of cash on hand, and that’s a very good thing. The company also has a fairly solid amount of shareholder equity compared to its minimal debt.

Not that all things are rosy here. This isn’t the 1990s, and we’re not judging the company based on what the expectation for an online retailer were then. That’s good because revenue growth isn’t near as easy to come by in this day and age.

The current level of shareholder equity puts the current price/book value at 1.92. That’s not terrible for a profitable company, especially with the collection of brands they come with. Unfortunately, Beyond is not a profitable company.

The Risks

The biggest risk for the online retailer is a failure to earn a profit. The company readily admits in its 10-K that Beyond has no specific, concrete plan for how to return to its former profitability any time soon.

The big obstacles to that come in the form of intense competition. Even combining Overstock and Bed Bath & Beyond, there are more and larger online retailers in the same segment. Also, important to remember is that while online retail has become a very serious business, the bricks and mortar operations are still a thing, and another former of competitors.

Advertising is also a big expense, and the company is very dependent on placement in search engines to attract customers. Getting good placement in the big search engines doesn’t come cheap, even if it is probably a fair bit more affordable than the old television commercials Overstock used to run.

As with everyone else, economic conditions also pose a risk. Beyond is reliant on consumer discretionary spending, and in the event of an economic downturn, they can expect that spending to be harder and harder to depend on.

Interestingly, one of the things Beyond emphasizes as a potential risk is their dependence on third-party carriers and insurers, along with independent fulfillment partners. It takes a lot of third parties to make the company function.

Beyond and Income, or Lack Thereof

|

2021 |

2022 |

2023 |

Q1 of 2024 |

|

|

Net Revenue |

$2.75 billion |

$1.93 billion |

$1.56 billion |

$382 million |

|

Gross Profit |

$624 million |

$443 million |

$314 million |

$74 million |

|

Net Income |

$389 million |

($35 million) |

($308 million) |

($74 million) |

|

Diluted EPS |

$8.11 |

(83¢) |

($6.81) |

($1.62) |

(source: 10-K from SEC)

Here is where we get into the meat of the questions about Beyond, as the company turned from appealingly profitable in 2021 into a much smaller retailer, and an unprofitable one at that. The question much become whether they can return to the 2021 levels, because if they do the company would be looking very cheap.

Unfortunately, the estimates for Beyond don’t look too encouraging on that count. Revenue is expected to slightly recover from 2023, going to $1.64 billion in 2024 and $1.96 billion in 2025. Sadly, the company is not expected to return to profitability, expecting to lose $3.42 per share in 2024, and another $1.02 per share in 2025.

That’s where the cash on hand becomes so important. The losses of the next two years, if the estimates are to be believed, weigh in at about $203 million. That’s a deep cut into the cash, but if it meant growing into a profitable company afterwards, it’s an expense that Beyond could bear.

Conclusion

The reality of the situation is, Beyond can be had for a premium of less than twice its book value, but without an avenue to return to profitability, they are really just spinning their wheels and waiting for something better to happen.

If one could’ve sold Beyond back in March, they would’ve been wise to do so. That ship has sailed, unfortunately, but I still have to consider this a sell, even at the more discounted rate of current days.

The era when online retailers could lose vast amounts of money indefinitely is over, and the pressure is truly on for them to prove they are able to piece together a going concern. Maybe they will, but at these levels, I certainly wouldn’t be willing to bet on it. The reward could be great, but the risks are simply too high.

Read the full article here