Trading natural gas is not or the faint of heart; there’s a reason trading natural gas is often called a ‘widow-maker’ trade. However, natural gas prices are also quite predictable in some ways as it is mostly based on supply/demand factors and human behavior. In April, I advised investors that seasonality was favorable for trading short-term natural gas products like the ProShares Ultra Bloomberg Natural Gas ETF (NYSEARCA:BOIL) into June.

Investors who followed my recommendation and bought the BOIL ETF on April 3rd (when my article was published) could have realized over 60% in total returns had they monetized at the peak in June (Figure 1).

Figure 1 – BOIL delivered over 60% in total returns from April to June (Seeking Alpha)

However, I also warned investors not to overstay their welcome, as the BOIL ETF is not for buy-and-hold strategies. If investors had held onto the BOIL ETF from April 3rd to today, they would have experienced negative total returns of -9.1%.

Unfortunately, a decline in value for the BOIL ETF is actually the norm due to the fund’s amortizing structure.

Brief Fund Overview

For those who are new to my articles or the BOIL ETF story, the ProShares Ultra Bloomberg Natural Gas ETF is a futures-based ETF that seeks to provide daily returns that are twice the return of the Bloomberg Natural Gas Subindex (“Index”). The index reflects the daily performance of a rolling position in front-month natural gas futures. As front-month futures contracts expire, the index mechanically replaces them with futures contracts with a later expiration.

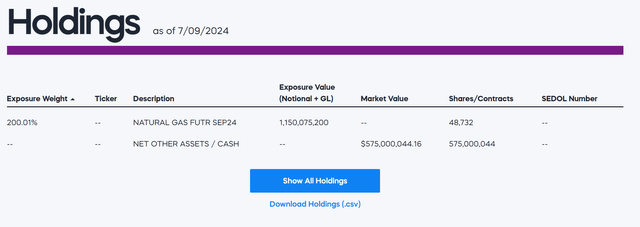

Figure 2 shows the current holdings of the BOIL ETF, which consists of 200% exposure to September 2024 futures and cash (Figure 2).

Figure 2 – BOIL fund holdings (proshares.com)

Not A Buy-And-Hold Fund

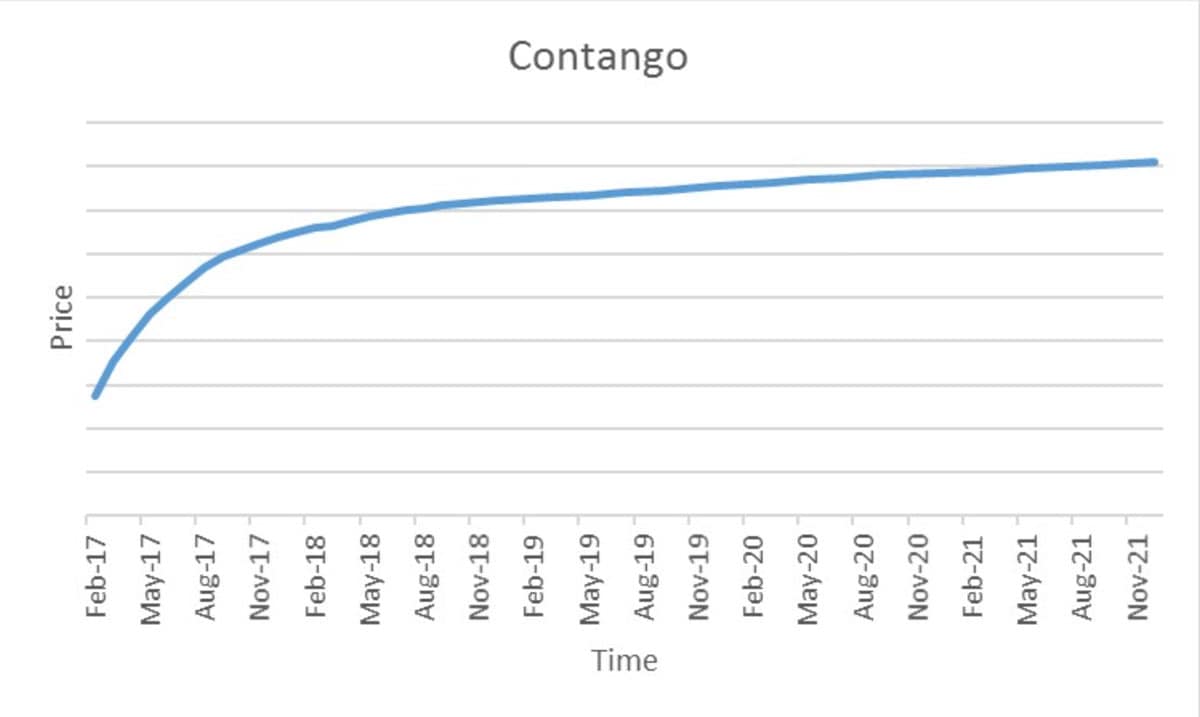

To reiterate my warning from the beginning of this article, the BOIL ETF is not suitable for long-term buy-and-hold investors. The main issue with the BOIL ETF (and other futures-based ETFs) is that future prices tend to be in contango, where prices farther out in maturity are more expensive (Figure 3).

Figure 3 – Ilustrative futures contango (CME)

So every time the near-month natural gas futures expire, the BOIL ETF must mechanically sell the expiring future at a lower price and buy a more expensive futures contract expiring at a later date as a replacement. This mechanical ‘futures roll’ process leads to the ETF suffering losses from ‘roll decay’ over time.

A second issue with the BOIL ETF is the fact that it is leveraged. Levered ETFs have ‘positive convexity’ in the direction of their exposure and ‘volatility decay’ as they must rebalance their levered exposures every night.

Using a mathematical example, assume an investor had invested $100 in BOIL. If the underlying index returns 5% on day 1, the position will grow to $110 (2 times 5% return). If the index returns -5% on day 2, the position will fall to $99, significantly less than twice the 2-day compounded loss of 0.25% or $99.50. This loss in value is called ‘volatility decay’.

Although ‘volatility decay’ is small on a day-to-day basis, for volatile assets like natural gas futures, the compounded slippage from volatility may be very significant.

Traders considering the BOIL ETF should ensure they fully understand the tracking error risks involved with levered and futures-based commodity ETFs by consulting these FINRA and SEC warnings.

Natural Gas Seasonality Explained

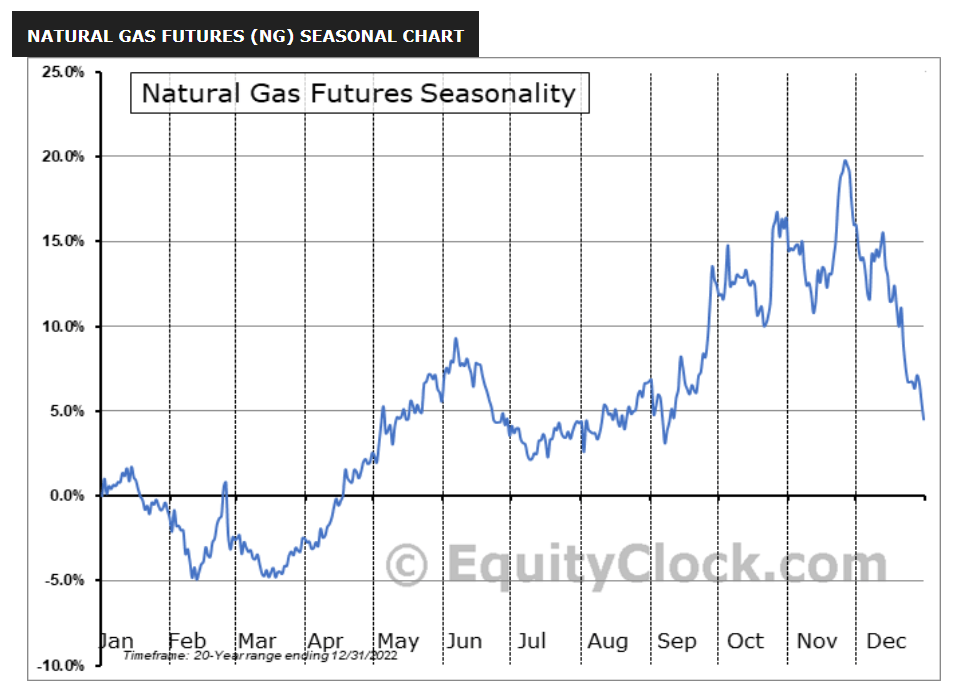

For those new to natural gas trading, natural gas spot prices exhibit strong seasonality because the fuel is not as transportable as crude oil, and the demand for natural gas is driven by speculation around the summer cooling season and the winter heating season (Figure 4).

Figure 4 – Natural gas exhibits strong seasonality (equityclock.com)

In a typical year, speculators start to bet on summer cooling demand around March/April, and the speculative frenzy reaches a peak in June, just as actual cooling demand is realized.

Then during the summer months of June and July, even though the weather may be very hot, spot natural gas prices tend to decline as reality is often not as bad as feared.

A similar process begins in August as natural gas traders begin to speculate about winter heating demand. Winter speculation reaches a peak in late November/early December, and declines as actual heating demand is realized in January/February.

While no two seasons are the precisely same, the general seasonality for natural gas prices is very pronounced and has rewarded me handsomely over the years.

Natural Gas Storage Pressuring Spot Prices

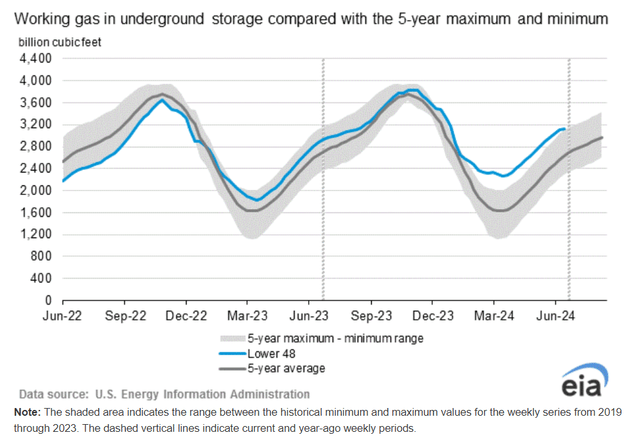

For now, I expect natural gas prices to remain soft for the next several weeks, as gas in storage has remained above the 5-year average due to strong production (Figure 5).

Figure 5 – Natural gas in storage above seasonal levels (EIA)

For investors looking to take a long swing trade on the BOIL ETF or other related products like the United States Natural Gas Fund (UNG), I recommend they be patient and reassess the gas markets in August/September, to see how much gas has been drawn to fuel the summer cooling season and the prospects for the upcoming winter heating season.

Watch For Signs Of La Niña In Coming Months

For natural gas speculators, the wild cards disrupting seasonality patterns may be climate change and El Niño/La Niña effects. For those not familiar, El Niño and La Niña are climate patterns in the Pacific Ocean that can affect weather patterns worldwide.

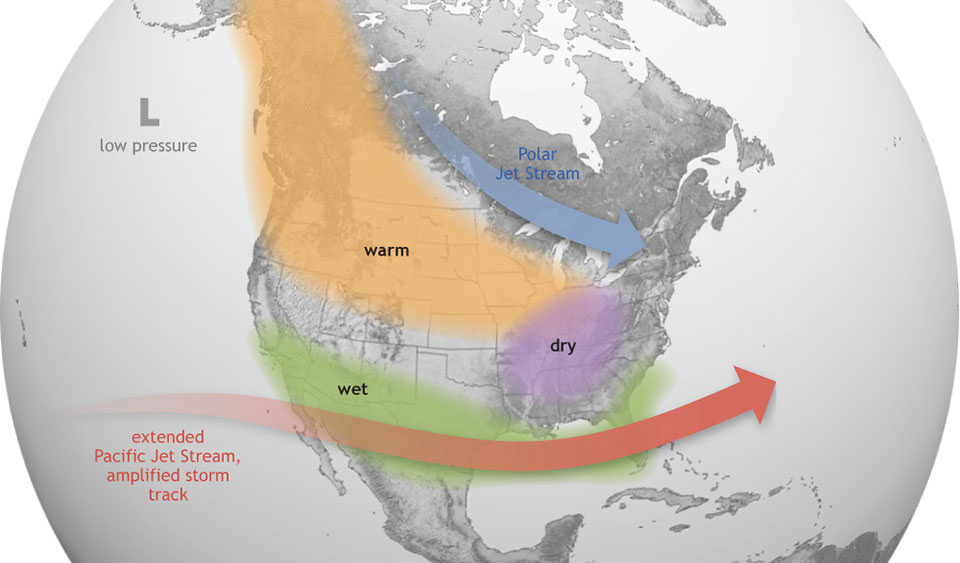

El Niño tends to cause dryer and hotter weather across the U.S. and Canada (Figure 6).

Figure 6 – El Nino weather patterns (NOAA)

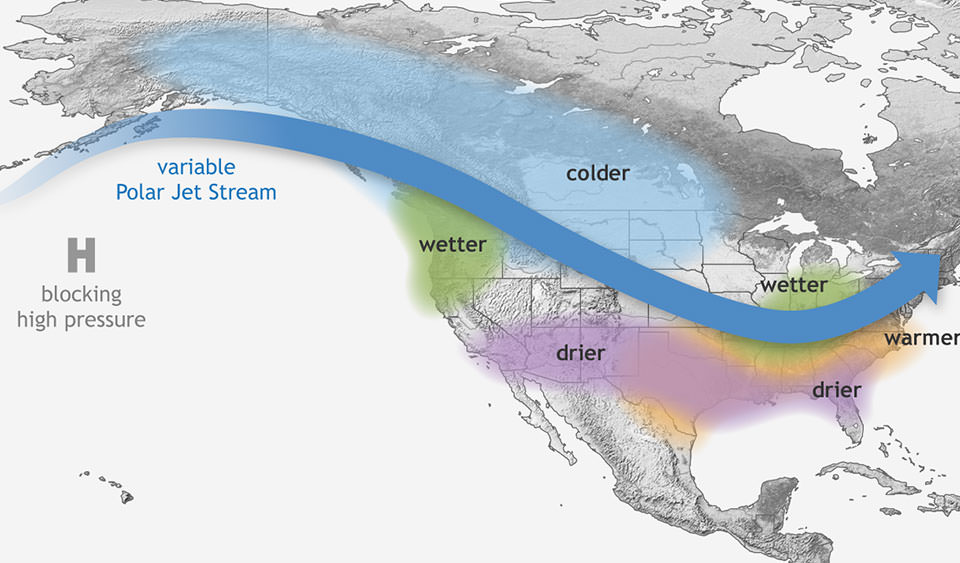

In contrast, La Niña brings colder and wetter weather to North America (Figure 7).

Figure 7 – La Nina weather patterns (NOAA)

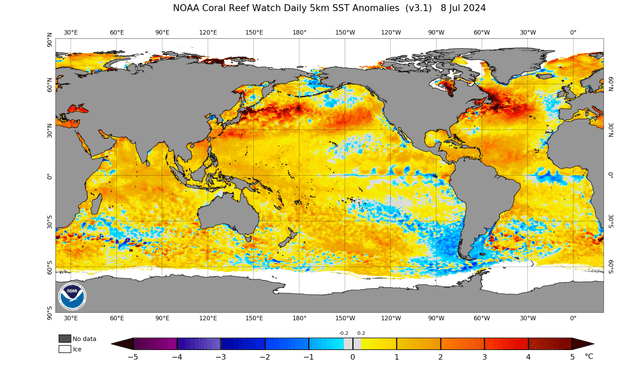

Last year’s El Niño was one of the reasons why the North American winter we experienced in 2023/2024 was one of the mildest on record. However, El Niño conditions recently ended with sea temperatures returning to normal (Figure 8).

Figure 8 – Sea temperatures are back to normal (NOAA)

Looking forward, according to the NOAA, there is a 65% chance that La Niña conditions may develop in the next few months. So investors looking to bet on a colder/wetter than normal winter season requiring more heating may want to keep a close eye on upcoming NOAA reports.

Conclusion

The bullish case for the BOIL ETF recently ended in June, as positive seasonality and El Niño conditions both concluded. Looking forward, I believe bullish investors need to be patient and wait for winter fuel demand speculation to start in late August/September before making another bet on BOIL.

This upcoming winter season could be fruitful, as there is currently a 65% chance of La Niña conditions developing for the upcoming winter season. Typically, La Niña winters are colder and wetter than normal, which could increase fuel demand. I rate BOIL a hold and will reassess in a few months.

Read the full article here