Investment thesis

Codere Online (NASDAQ:CDRO) has seen its share price double this year due to strong revenue growth and improving profitability. The company has a recognized brand name with an omnichannel presence, which gives it an edge in acquiring customers versus its competitors. After the recent share price appreciation, I believe the risk-reward is no longer favorable for investors, considering the risk for material downside mainly due to regulatory and competitive threats. Therefore, I believe it is prudent to wait and better understand how these risks are playing out in the upcoming quarters.

Business Overview

Codere Online is a B2C online gambling operator which offers its customers sports betting and casino games. It was spun off from Codere Group via SPAC IPO in December 2021. Codere Group remains the company’s largest shareholder, and has been involved in operating brick-and-mortar gambling venues since 1980 with a significant presence in Spain and later Latin America. Codere Online’s presence online coupled with Codere Group’s retail presence gives the brand an omnichannel presence in its main markets. Additionally the Codere brand is the official betting partner of the Monterrey Rayados Football Club in Mexico as well as the main Sponsor of the women’s team, Rayadas.

Today Codere Online has licenses and operates in multiple markets which include Spain, Mexico, Colombia, Panama, Chile, Uruguay and the City of Buenos Aires. The company however has stated that it has no plans to enter the recently regulated Brazilian market.

Mexico remains the company’s most significant market, and it is among 15 other operators in the country, which include its largest competitor, Caliente. According to a research report by ENV Media, gaming revenues in Mexico is estimated to be close to $1.9 billion for 2023, with double digit growth rates forecasted until 2028.

Achievements in recent quarters

By leveraging its well known brand name and strong financial position after its IPO, Codere Online has rapidly scaled and grown its revenues. Furthermore, the company has also benefitted from its first mover advantage and market tailwinds. In the sections below, I will walk through some of the key achievements the company has made in recent quarters, as well as how the trends look going forward.

Strong revenue growth

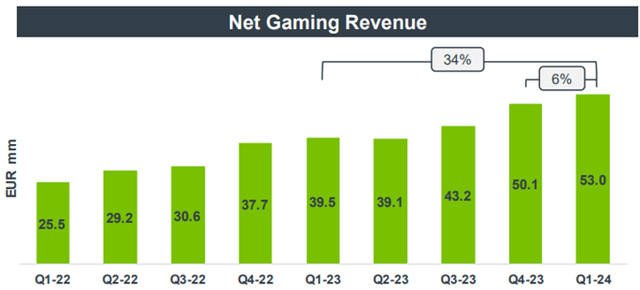

Company presentation

Codere Online has shown strong growth, with quarterly revenue in Q1 2024 nearly double the amount from two years ago, as shown above. The 34% year over year growth is mainly attributable to the growth in Mexico, which was above 50% in Q1 2024. Management’s guidance for full year revenue, which is likely conservative, calls for a deceleration in growth to 18%. Analyst estimates are much higher, implying a growth rate of 23%. Revenue growth should be further supported by football events such as the Euro Cup and Copa America later this year. With strong tailwinds in the markets that it operates in, I expect the company to maintain a double digit growth in the next five years.

Improving profitability

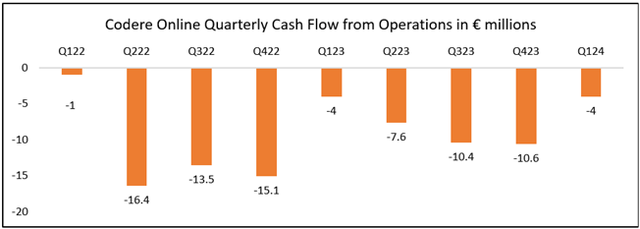

Created using company data

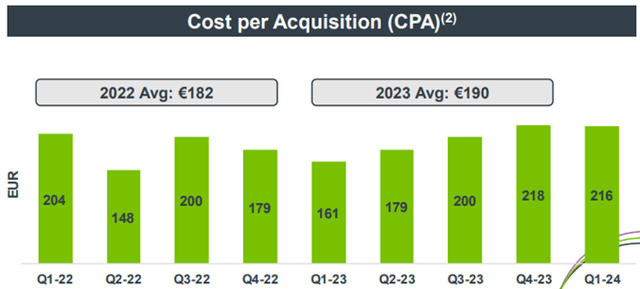

As depicted above, despite showing heavy cash burn during the last two years in its attempt to gain market share and drive growth, the company has in recent quarters improved its profitability and aims to be FCF positive this year. According to me, the main reason for Codere Online being able to grow profitably in a very competitive environment is its ability to keep its Customer Acquisition Cost (CAC) or what it refers to as CPA very low. As shown in the image below, despite revenue growing at a CAGR of almost 50% in the past two years, the CPA has only grown at a CAGR of around 15%. I believe the company has been able to leverage its omnichannel presence to acquire new users much more profitably compared to its competition.

Company presentation

My valuation model

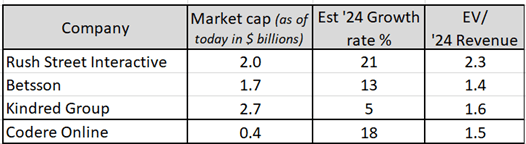

Since the company is in its early stages of growth and is only expected to turn profitable this year, metrics such as EBITDA and Free Cash Flow (FCF) are less relevant. I assume Codere Online will be able to reach margin parity with its peers such as Rush Street Interactive (RSI), Betsson AB (OTCPK:BTSBF) and Kindred Group (OTC:KNDGF), which operate in similar markets. Their EV to Sales ratios can be used as to compare the Codere Online’s valuation on a relative basis.

Created with data from Seeking Alpha

As seen from the table above, it is evident that the company is attractively valued considering its current growth rate as well as its future growth potential. When netting out Codere Online’s net cash of €33 million (around $36 million), it has an enterprise value of $330 million at a share price of $8, which implies an EV/S ratio of 1.5. According to me, this business’s valuation should be closer to Rush Street Interactive, which is also a significant player in the Mexican market. If Codere Online’s EV/S ratio were to re-rate from 1.5 to 2, its share price would be $10.5 which is an upside of at least 30%.

Potential catalysts for further upside

Buyout from a larger player

Codere Online has a strong position and its brand is well recognized due to its parent Codere Group’s history in the physical gaming business. This together with its undemanding valuation, make it an attractive acquisition target for larger players looking to enter Mexico and the South American market.

Capital return to shareholders

With more than €30 million in cash and the business expected to be FCF positive this year, the company could potentially return capital to shareholders, likely in the form of dividends.

Risks which I think investors should consider

Regulatory changes

The company is susceptible to regulatory changes made by the governments in the regions where it operates. For instance, in Spain, a decree was enforced banning aspects of certain advertising by gambling operators, such as sponsorship deals. These types of restrictions can severely hinder Codere Online’s ability to acquire new users to its products.

Competition

The strong growth in its Mexican market is likely to attract more competitors, and this was highlighted by CEO Aviv Sher during the Q1 earnings call when he said:

Well, we do see competitors coming in as they said they will do during this year. We see Betano coming in very, very strong with a lot of marketing investment into Mexico in some kind of partnership with Azteca, a local TV station. Yes, I think the competitive landscape in Mexico changes. We know our main competitor keeps growing, same as we are. We keep growing. So the market is growing, but more and more competitors are coming in.

Large owner undergoing restructuring

More than 60% of Codere Online’s shares are held by Codere Group, which has been struggling and was restructured last year due its high debt load. Though it is yet to happen, the possibility of its largest owner liquidating a significant portion of its shares in Codere Online is an overhang on Codere Online’s share price.

Indirect holding of Mexican license

Codere Online’s license to operate in Mexico is valid until May 2027 and is held by its wholly owned subsidiary LIFO (Libros Foráneos, S.A. de C.V) according to its 2022 Annual report. Any issues which could threaten LIFO’s existence such as insolvency could lead to Codere Online losing its license to operate in Mexico.

Revenue concentration in the Mexican market

A major portion on Codere Online’s revenue is derived from the Mexican market. In its recent quarter, this was as much as 50% of the total revenue. Any changes in the competitive or regulatory landscape in the country could have adverse impacts on the company’s business.

Delay in Annual report

The company has notified the SEC that it will not file its 2023 Annual Report on time. This is because it has changed auditor earlier this year. Since no timeline has been mentioned for the filing, investors should track this closely to ensure that there is no risk for the misstatement of any of its prior financials.

Conclusion

Codere Online shows a promising growth story and benefits from market tailwinds. Nevertheless, it trades at a discount to its peers when considering its growth potential. On the other hand, I believe significant regulatory and competitive threats still remain in the industry and the markets that the business operates in, which could lead to material downside for investors. At today’s share price, I believe the risk-reward warrants a Neutral stance towards Codere Online as an investment.

Read the full article here