Investment Thesis

Crescent Point Energy (NYSE:CPG)(TSX:CPG:CA) has transitioned after the Hammerhead Energy acquisition and ended up with a premium 20+ years drilling inventory portfolio. The acquisition increased the company’s share count and debt, and investors didn’t take it well. While most Canadian O&G (Oil and Gas) producers are now deleveraged and focus on returning the capital to shareholders, Crescent needs to focus on debt repayment again. CPG also has a gassier production profile now with 65% liquids production, down from 76%. I don’t see it as an issue, as I am equally bullish on gas and oil.

The company has strong production growth ahead, targeting 2028 production levels of 260.000 BOE/d (Barrel of Oil Equivalent per Day), up from 159.408 BOE/d for 2023. While the company significantly grows its production, it is still expected to generate about C$800M of excess cash flow in 2024 (13% yield), with 40% used for debt repayment and 60% for the combination of dividends and buybacks.

The oil price is well positioned in the high seventies with OPEC’s recently confirmed production cuts, and the debt is conveniently sitting on a D/CF of 1.2 (US$75 WTI). Traditional metrics like next year’s EV/DACF do not show the undervaluation. Still, if I make a 5-year DCF projection and fully utilize the planned growth in the equation, I will find a fair value of C$18.66 per share, which points to a potential 84% upside. Right now, I consider it the best buy in the Canadian O&G space and place a Strong Buy label on the stock.

Transformed Crescent Point Energy

After the Hammerhead Energy acquisition, during the most recent call, Crescent’s management answered the question about future acquisitions like this: “As far as acquisitions, we’re not going to be doing anything on that front. So, on the acquisitions, I would say no.” It is also confirmed by Crescent recently passing on the potential buy of Duvernay shale assets put on sale by Chevron.

The newly acquired assets from the Hammerhead were adjacent to Crescent’s operations. Thus, I believe that management knows what they are buying well. Their drilling portfolio increased to 20+ years, providing them with strategic infrastructure ownership and scalable market access.

Crescent comes into 2024 with new gassier assets, higher debt, and a higher share count. While nobody likes issuing new shares, I think the management made a good deal by buying Hammerhead. It improves the FCF per share outlook if you are okay with waiting a few years for higher payouts after deleveraging. Taking some debt as a lower-cost producer, like Crescent, is no issue, in my opinion. Gassier assets are also fine with me as I am quite bullish on gas as the LNG export from NA is expected to double by 2027, increasing demand and driving up prices, as I explained in my ARC Resources article.

Crescent’s Assets (Crescent Presentation)

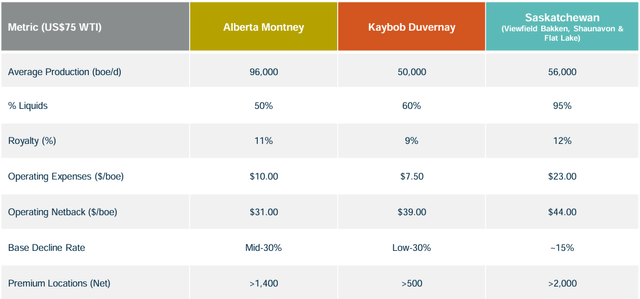

Crescent is allocating about 45% of the 2024 budget to its Montney assets, focusing on enhancing the well’s design and expecting to grow the production by 40% by 2028. 35% of the budget will be allocated to Duverney assets, where production is expected to grow by 50% by 2028. Saskatchewan assets are in a slow production decline supported by water and polymer flooding. It is positioned close to the US borders, providing a market access advantage. These are their highest netback long-generating assets. Crescent allocates 20% of its 2024 budget here.

Crescent Production Profile (Crescent Presentation)

Observing their future production, we see a higher portion coming from gassier Montney and Duverney with a much higher production base decline. While Crescent currently grows with a capital spending of C$1.5B, it won’t be enough in 2028 as it will be just enough money to offset the decline.

2023 Results

In 2023, the company produced 88,087 bbls/d of Oil, 15,026 bbls of NGLs, and 211,275 mcf/d of natural gas, representing 21% production growth, which was in line with expectations. The revenue was down to C$4.1B because of a lower oil price environment than last year.

With an average pricing of US$77.6 WTI and C$2.93 AECO, the company generated an excess cash flow of C$980M and is projected to generate an excess cash flow of $830M in 2024 at US$75 WTI. C$600M was returned to shareholders via dividends and buybacks, representing about 60% of excess cash flow in line with the planned payout ratio for 2024.

They ended the year with a net debt of C$3.74B. While this only represents a D/CF of 1.2, the management prioritizes the debt repayment, allocating 40% of excess cash flow until its repayment is lowered to C$1.5B, where management will consider increasing the shareholder payout ratio.

While recently boosting the dividend by 15% to a current yield of 4%, the management clearly stated that they are not planning any special dividends but prefer to buy back their stock, which I like due to no taxation.

Valuation

2P NAV valuation (Net Asset Value of Proved and Probable reserves)

Investors received Crescent Point’s 2P NAV valuation based on independent engineering pricing. It stands at C$22.45 per share at year-end 2023, only accounting for 30% of Montney and 60% of Duvernay’s assets. While this points to high undervaluation, most Canadian O&G producers are undervalued based on their 2P NAV. To decide if I want to invest, I care not only about the value but mainly how shareholders will benefit.

Quant

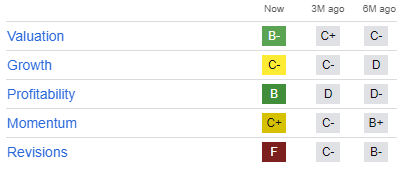

The quant rating points to “Hold”. The issue of quant with commodity companies is that it needs to focus on the right metrics. In the short-term, the revenue and profits are driven by movement in commodity prices, and since oil prices moved down, the quant shows negative numbers. We have to focus on production growth, improvements in operation efficiency, FCF generation, etc.

SA quant (Seeking Alpha Quant)

Projecting the next five years for DCF valuation

To assess the intrinsic value, I am making a future projection with a DCF (Discounted Cash Flow) valuation. I am assuming guided production levels by management, US$75 WTI oil prices, a consensus among most large analysts, and C$3.5 AECO prices currently reflected in futures prices. I do not consider any gains or losses from hedging, as it may be important in near-term numbers but close to irrelevant in long-term projections. The 2023 FCF is shown as negative due to the cost of the Hammerhead Energy acquisition.

5 years projection (Author’s Calculation) 5 years projection (Author’s Calculation)

DCF valuation

As a discount rate, I use a WACC (Weighted Average Cost of Capital) calculated from the pre-tax cost of debt of 5.4% and the cost of equity of 12.5%. The final WACC stands at 9.35% and increases to 10.77% in 2028 due to higher financing from equity caused by company deleveraging.

DCF valuation (Author’s Calculation)

I then discount the dividends and buybacks by the WACC. The discounted cashflows per share for the next five years equals C$4.02. The terminal value is based on the final year maintenance FCF of C$1.8B. After discounting, I arrive at the terminal value of C$14.64 per share.

Put it together, you arrive at a fair price of C$18.66 per share, which, compared to today’s price of C$10.15, stands at an 84% upside.

Shareholders yield

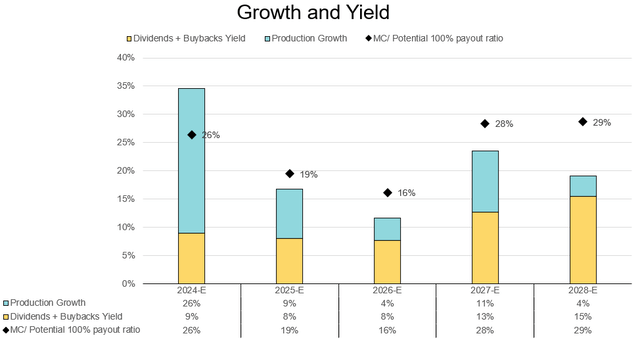

Put it simply and see the yield for yourself. Shareholders will be rewarded by the production growth, dividends, buybacks, and debt reduction. The management can decide to boost the payout ratio anytime, but they mentioned that they feel convenient with C$1.5B debt. Keeping the current 60% excess cash flow paid via dividends and buyback will yield 15% in 2028. If the management does not spend for further growth and keeps the remaining debt constant, they could start paying a 29% yield in 2028.

Growth & Yield (Author’s Calculation)

Risks

The first thing to come to mind is that the company works with newly acquired assets. Since these assets are adjacent to Crescent’s older assets, I believe the engineers made correct estimations about future growth, but this remains a risk. Even though we know the growth plan, I hope the management will show more details in the upcoming presentation on 20th March.

The stock is cheaply priced, meaning investors do not want management to perform some risky growth. Investors will be well rewarded if the management performs according to a plan. If it comes to any new acquisitions and changing strategies, I believe investors would not be happy and could create selling pressure on the stock.

The company has approx. 75% of its debt with floating rates, and the interest rate rose to 5.4% from 4%. Even though the debt is higher compared to peers, it’s still easily managed with a D/CF of 1.2. Crescent is also hedging 35-40% of its production, so if oil prices drop, the company would still make enough money to cover the debt payments.

One thing that concerns me is the rising base decline rate. Once the company achieves the 2028 production plan, C$1.5B will be just enough to offset the production declines and will not bring any further growth.

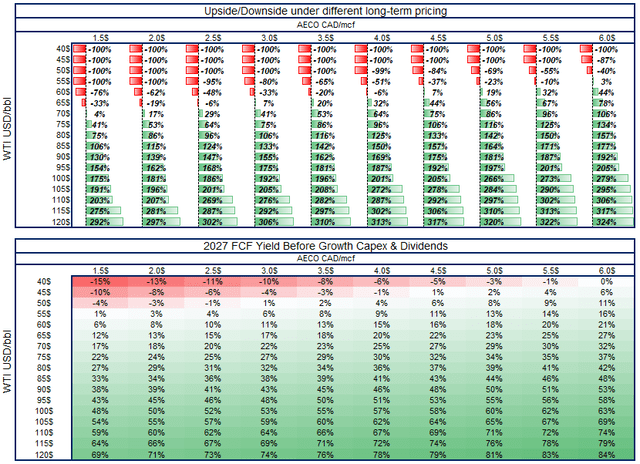

The main risks with any O&G producer are the commodity prices. I will now conduct a sensitivity analysis under different O&G prices to determine prices under which the company remains profitable and how the company’s value changes.

The first heat map shows the upside to the intrinsic value under different O&G prices, assuming keeping the current growth plan. The downside could be represented better because, with lower long-term prices, the company would change its strategy to stay profitable.

The second table represents its 2027 FCF yield before spending for growth and debt repayment. The company is still expected to be FCF-positive even under an oil price of US$50WTI and gas AECO C$3.

Sensitivity analysis (Author’s Calculation)

Investment Decision

Pros:

- Crescent Point came through a transition and now owns 20+ years of drilling portfolio.

- The production is growing fast, with a target of 260.000 BOE/D in 2028 compared to 159.408 BOE/D in 2023.

- Crescent repays its debt while 60% of excess cash flow goes to shareholders via dividends and buybacks.

- The management confirmed they are not interested in any further acquisitions, making a clear path for shareholders’ returns.

- The company can sustain its production levels while staying profitable even with prices of US$50 WTI and C$3 AECO.

- Structural improvements in LNG export from NA creates a better price environment for NA gas prices.

- Recent OPEC cuts support the oil price. With expected US shale production declines, the future for oil prices is bright.

Cons:

- The production is growing gassier, lowering the production margins.

- Gassier production will have higher decline rates; thus, the Capex needed to offset those declines will grow.

- The company can sustain its production levels while staying profitable even with prices of US$50 WTI and C$3 AECO.

- Newly acquired assets bring higher operational risks.

Price is what you pay, and value is what you get. Based on detailed DCF valuation, the gap between those two is too wide for Crescent, pointing to an 84% upside in share price or 20%+ yearly returns if oil prices do not fall, which makes me rate the stock as a Strong Buy.

Two weeks later, Crescent will hold a conference call, hopefully revealing more details on the operations execution strategy. Remember to subscribe and not miss any future updates affecting the investment thesis. Let me know in the comments if you have a different view of the company or see similar opportunities in the energy space.

Read the full article here