Investment thesis

My previous bullish thesis about Crown Castle (NYSE:CCI) did not age well as the stock declined by around 10% since December 2023. The weak sentiment around the stock is due to the expected to deteriorate in Q1 and full fiscal 2024 financial performance. However, the major portion of the decline is expected by the last year’s one-off favorable factors together with non-cash accounting entries of 2024. With the effect of these one-off events eliminated, CCI is expected to continue demonstrating organic growth. My valuation analysis suggests that the stock is currently around 30% undervalued. Moreover, after a recent pullback, CCI currently offers a compelling 6.5% forward dividend yield. Readers should keep in mind that it is not a short-term play, but a solid dividend opportunity. All in all, I reiterate “Buy” rating for CCI.

Recent developments and earnings preview

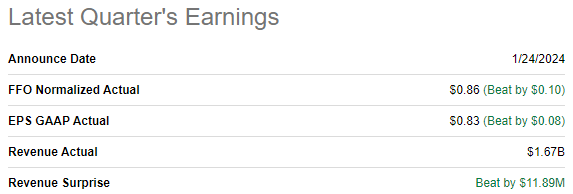

The latest quarterly earnings were released on January 24, when CCI surpassed consensus estimates. Revenue declined by 5.1% YoY, and the FFO followed the top line by shrinking from $1.93 to $1.82.

Seeking Alpha

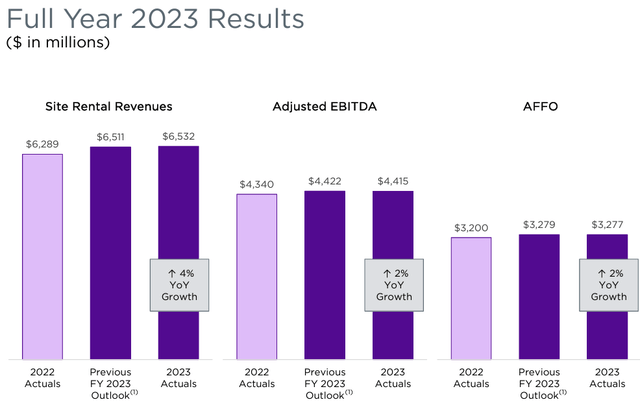

Despite the revenue and FFO decline in Q4, for the full fiscal 2023 CCI’s performance was decent [considering the challenging macro environment] with revenue and FFO demonstrating modest growth. Despite being modest, the growth looks reasonable considering the high penetration of the industry.

CCI’s latest earnings presentation

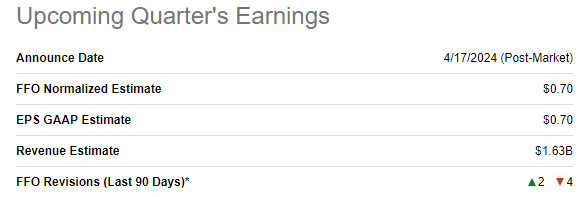

I am not paying much attention to the latest earnings release because Q1 earnings release is approaching and scheduled on April 17. Wall Street analysts’ consensus expect quarterly revenue at $1.63 billion, which indicates a 7.9% YoY decrease. The FFO is expected to decrease significantly, from $1.92 to $0.70.

Seeking Alpha

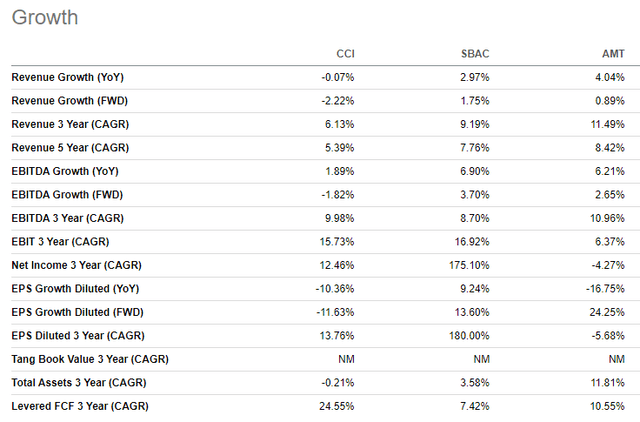

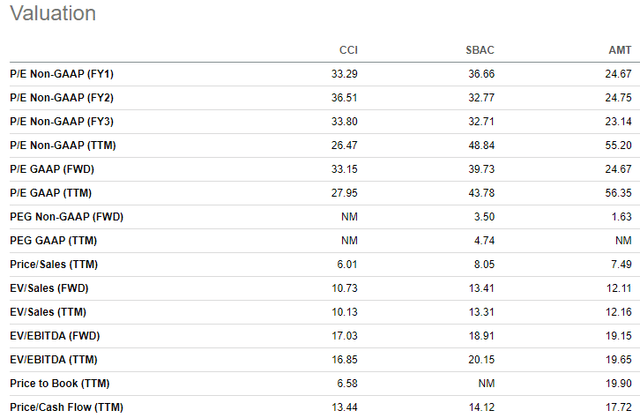

Overall, there are three major factors which the management expects to weigh on CCI’s financial performance in 2024. First, received $170 million Sprint cancellation payments in 2023, which will not recur in 2024. Second, the expected $250 million adverse effect is expected due to non-cash items related to amortization. Third, a $55 million lower contribution from services gross margin is expected. According to Dan Schlanger, the CFO, if the effect of these three items is eliminated, site rental revenues, adjusted EBITDA and AFFO would show year-over-year growth of 4%, 5% and 3% respectively. Compared to peers like American Tower Corporation (AMT) and SBA Communications (SBAC), CCI’s adjusted growth figures look much better than AMT and SBAC forward revenue and EBITDA growth.

Seeking Alpha

Therefore, it looks to me that Q1 2024 challenges are temporary and we should not lose the forest for trees. When I invest, I prefer to look more at the dynamics of key business metrics, which are expected to expand in 2024. The company’s geographic footprint and scale are substantial, which makes CCI well-positioned to absorb industry tailwinds which includes the expected demand growth for more connectivity as our world continues digitizing at rapid pace.

CCI’s latest earnings presentation

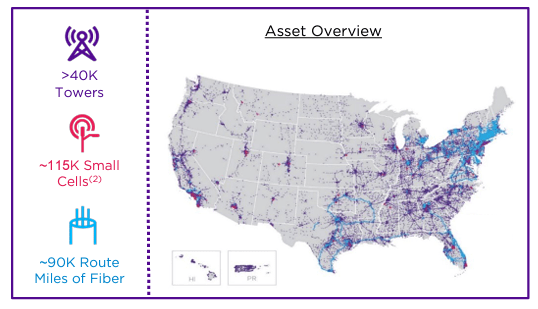

I expect CCI’s shared communication infrastructure, which comprises more than 40 thousand cell towers and approximately 90 thousand route miles of fiber to enable the company to generate consistent and predictable FFO over the long term. This adds to my confidence that the dividend is safe and will highly likely continue demonstrating above-the-inflation growth over the long term.

I think that pessimism around the upcoming earnings release is already priced in and CCI might be a good play before earnings. The company had a weak earnings surprise history several years ago, but in recent quarters disappointing figures were rare. That said, CCI is able to deliver above the consensus performance in Q1 and the pessimism is already priced in the cautious forecasts.

Valuation update

CCI declined by 28% over the last twelve months and had a difficult start in 2024 with a 16% YTD decline. CCI’s price-to-FFO ratios look in line with the sector median, meaning that CCI is about fairly valued. Compared to the closest peers, AMT and SBAC, CCI’s valuation ratios also look reasonable.

Seeking Alpha

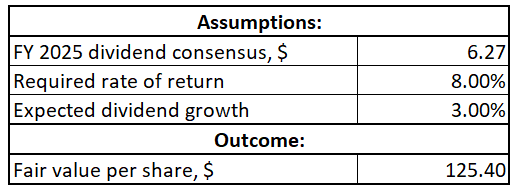

Now let me proceed with the dividend discount model [DDM]. Due to still high inflation in the U.S., I reiterate the same 8% required rate of return, which also aligns with the range recommended by valueinvesting.io. Since I am calculating target price for the next 12 months, I use FY 2025 dividend consensus forecast, which is $6.27. I reiterate the same 3% dividend growth rate for my DDM, this aligns with the last three years’ AFFO CAGR.

Author’s calculations

According to my DDM simulation, CCI’s fair share price is $125. This is 30% higher than the last close, meaning that CCI is substantially undervalued. Let us look at risks of investing in the stock to understand whether the upside potential is worth all the risks and uncertainties.

Risks update

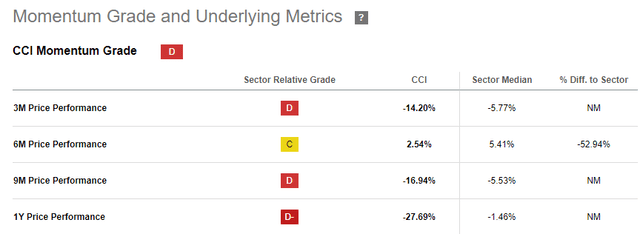

I think that CCI is not a short-term play for investors who are seeking for share price spikes on short timeframes. As I mentioned above, the company’s financial performance is expected to deteriorate in 2024, which is a negative catalyst for the stock price. The market sentiment around CCI is mostly negative and the momentum is weak across various timeframes. This means that a sharp turnaround in the share price is very unlikely, and it might continue stagnating. Investors who will eventually decide to opt in should be ready for the weak share price dynamic and ready to keep shares for longer.

Seeking Alpha

The uncertainty around the Fed’s monetary policy also might not add optimism in the short term. In early April, there was a public speech from the Fed’s Chairman, Jerome Powell, who said there is no rush to cut rates. I consider this as a hawkish message, which was amplified last week by the hot March CPI data. Since CCI is a highly-leveraged business [which is inherent to the industry it operates], tight monetary policy is a headwind for the company. However, it is crucial to understand that monetary policy is cyclical and softening phase of the cycle is just a matter of time.

Bottom line

To conclude, CCI is still a “Buy”. The company is expected to record a decline in its financial performance in Q1 and full 2024, but these are temporary and not secular issues. The good part is that the business continues demonstrating organic growth, which makes future more predictable. The stock is around 30% undervalued and currently offers a high 6.5% dividend yield.

Read the full article here