Introduction

It’s time for another article on natural gas. This year, I have given this industry a lot of attention, as I believe the current natural gas bear market offers tremendous opportunities in light of long-term tailwinds.

In recent weeks, I have covered three of my favorite four natural gas producers:

- ARC Resources (ARX:CA): A great Canadian producer with industry-leading breakeven prices and an eye on buybacks.

- Antero Resources (AR): An Appalachia-focused producer with low breakevens and deep reserves that favors buybacks over dividends.

- Range Resources (RRC): this company is a driller similar to AR, with the main difference being that it hedges its production and pays a dividend.

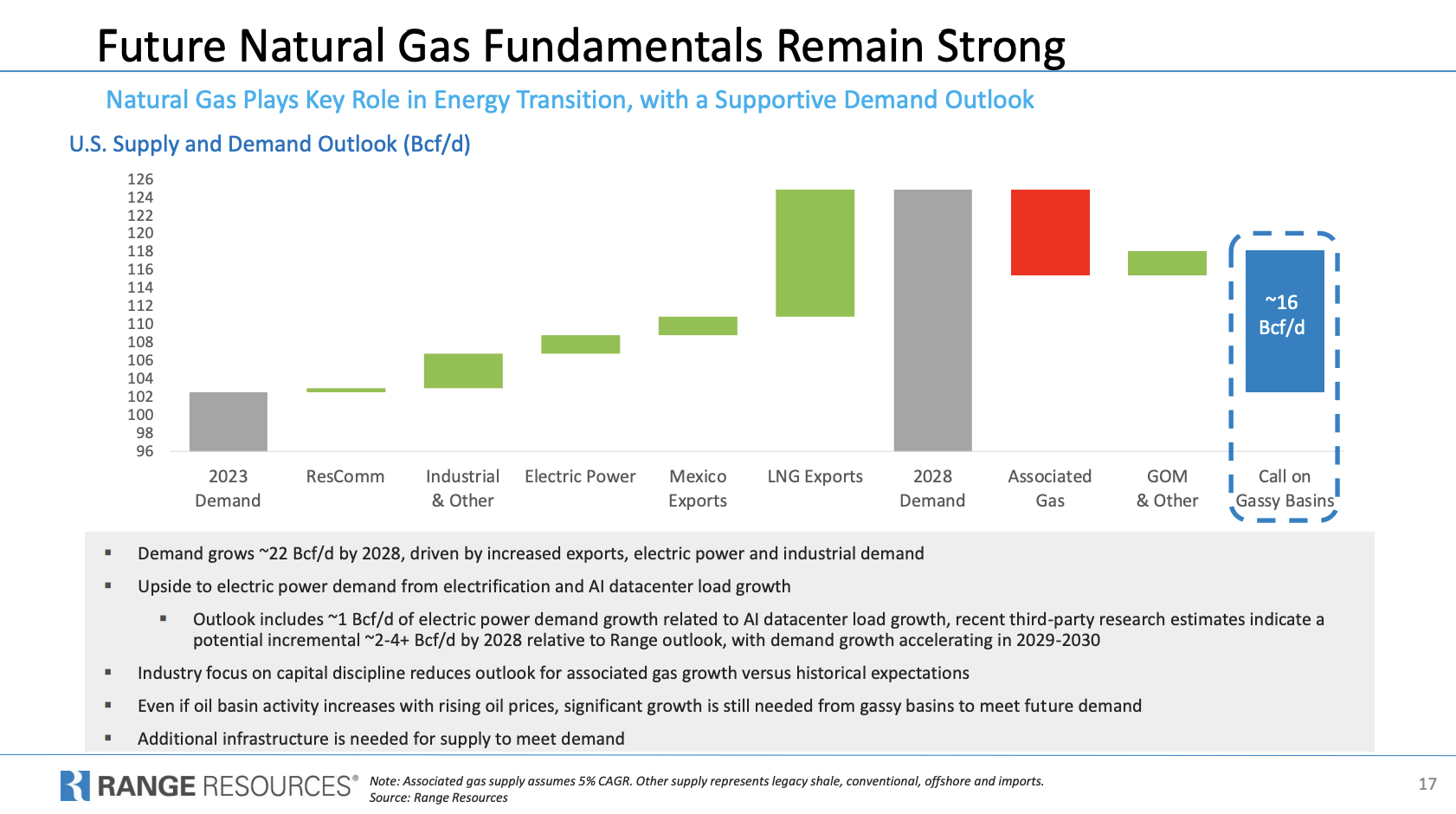

Although the operating environment is currently very tough, as Henry Hub natural gas is trading close to $2 again, there is hope on the horizon. This includes expectations for a 16 billion cubic feet per day supply shortage in the United States by 2028, fueled by accelerating LNG exports, industrial demand, and data centers.

Range Resources

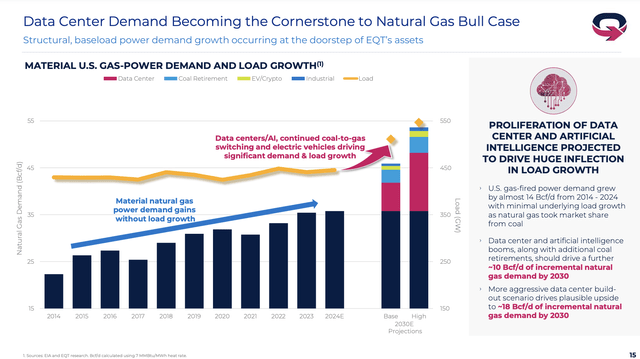

This is supported by EQT Corp. (EQT), one of the world’s largest natural gas producers. Using EIA and in-house research, the company estimates that U.S. gas-power demand could surge from currently roughly 35 billion cubic feet per day to almost 55 billion cubic feet per day in 2030, mainly fueled by data center demand and coal plant retirements.

EQT Corp.

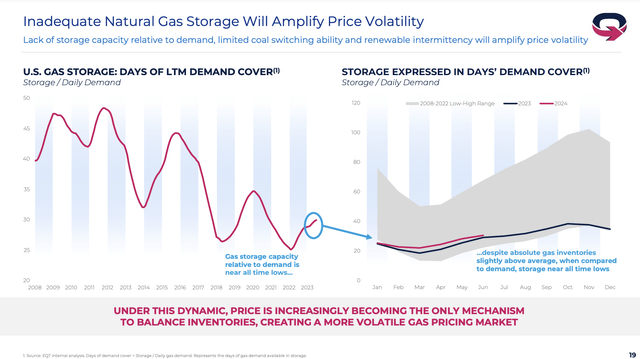

EQT also noted that while storage levels have risen (this is bearish), inventories are low when compared to rising demand.

EQT Corp.

These numbers mean that the price of natural gas is now extremely sensitive to supply and demand shocks, which makes the risk/reward quite attractive.

Natural resources investor company Goehring & Rozencwajg agrees. This is the quote I used in my Range Resources article:

While delays such as this postpone one source of new short-term demand, our medium term outlook remains unchanged. U.S. natural gas trades at an 84% discount to its energy equivalent, making it the cheapest molecule of energy on the planet. Gas for delivery in Europe remains $12 per mcf, while Asian LNG fetches $13.50 per mcf, compared with $2.00 in the U.S. As new LNG demand comes online and production continues to disappoint, inventories will continue to tighten, pushing prices towards the global benchmark. We cannot recall a more asymmetric investment opportunity than U.S. natural gas. – Goehring & Rozencwajg (emphasis added)

This brings me to the fourth natural gas play I like.

That company is the Tourmaline Oil Corp. (TSX:TOU:CA). If I had to describe the company the same way I summarized the other three picks at the start of this article, I would say something like “Tourmaline has the industry’s biggest reserves, low breakeven prices, and a focus on special dividends.”

The only article I’ve ever written on this company was published on June 27, 2023. Back then, it was a two-ticker article with its peer Antero Resources.

In light of my bullish view on natural gas, I will use this article to explain what makes Tourmaline such a powerful natural gas stock, especially for those seeking (special) dividends.

So, after a lengthy intro, let’s get to it!

Why Tourmaline Is Such A Special Stock

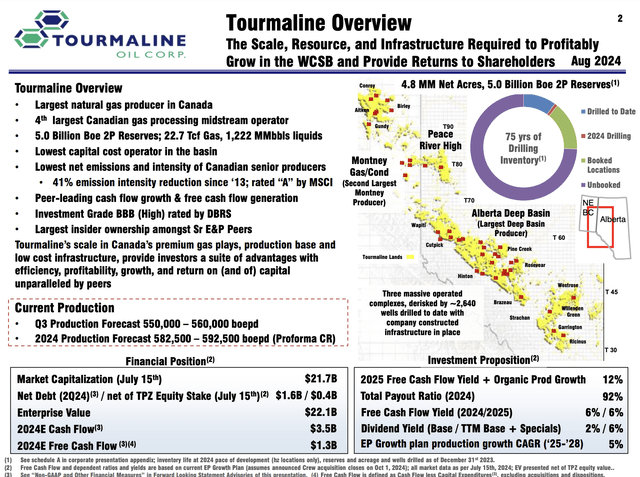

With a market cap of C$21 billion in Toronto, Tourmaline Oil is one of the biggest natural gas producers in the world. Although its name suggests it is focused on oil production, the company is the largest natural gas producer in Canada and the fourth-largest gas processing midstream operator.

It operates in the Western Canadian Sedimentary Basin, one of the biggest oil and gas basins in the world.

In this area, the company has 75 years of drilling inventory, which is unmatched by any oil and gas company I have ever researched – and I have covered many!

Tourmaline Oil Corp.

Moreover, the company, which has an investment-grade credit rating of BBB from Morningstar DBRS, generates a substantial amount of its revenue from high-margin natural gas liquids.

As we can see below, the company is the third-largest producer of conventional liquids, the largest producer of natural gas liquids (NGLs), and the second-largest producer of condensate in Canada.

The biggest difference is that NGLs consist of ethane, propane, butane, and pentane. Condensate is a liquid hydrocarbon mixture that forms when natural gas is cooled or put under pressure.

Tourmaline Oil Corp.

Last year, the company produced 119 thousand barrels of liquids per day. That number is expected to grow by 5% per year to almost 180 thousand barrels per day by 2027.

In 2Q24, the company’s production averaged 562 thousand barrels of oil equivalent per day, 13% more compared to the prior-year quarter.

On top of that, the company acquired Crew Energy in a deal close to $1 billion. This significantly boosts Tourmaline’s operations in the Montney shale formation in Alberta. This formation accounts for roughly half of Canada’s natural gas production.

Because of the deal, Tourmaline will become the largest producer in the Montney formation and unlock significant synergy potential of up to C$400 million.

Tourmaline Oil Corp.

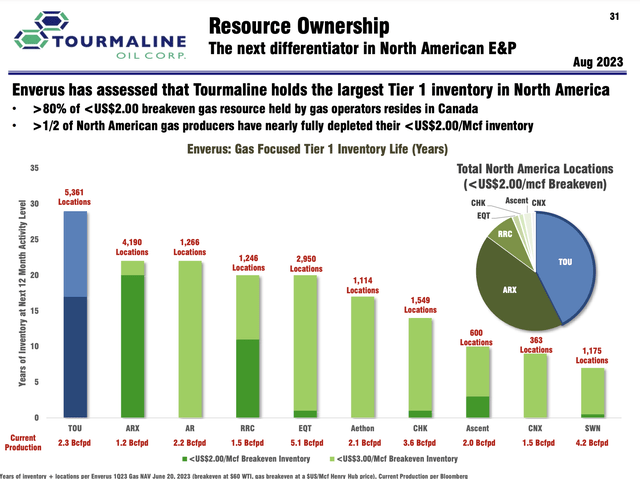

In general, the company has the biggest low-cost reserves in North America. Although ARC Resources has more inventory breakeven below $2.00 Henry Hub, Tourmaline has the biggest inventory when including inventory breakeven below $3.00.

Interestingly enough, the Enverus data below also shows that ARC Resources and Tourmaline own almost all production breakeven below $2.00!

Tourmaline Oil Corp.

As such, the company is in a great spot to boost its production.

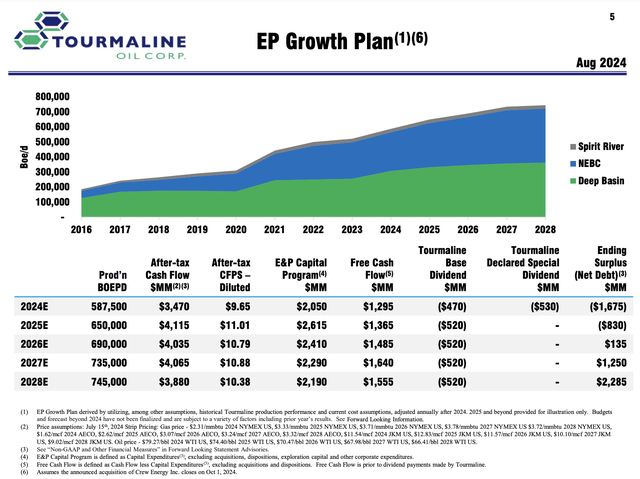

By 2028, it is looking to produce roughly 745 thousand barrels of oil equivalent per day, 27% more than its 2024 guidance. By then, it also expects to sit on more than C$2 billion of net cash (more cash than gross debt).

Tourmaline Oil Corp.

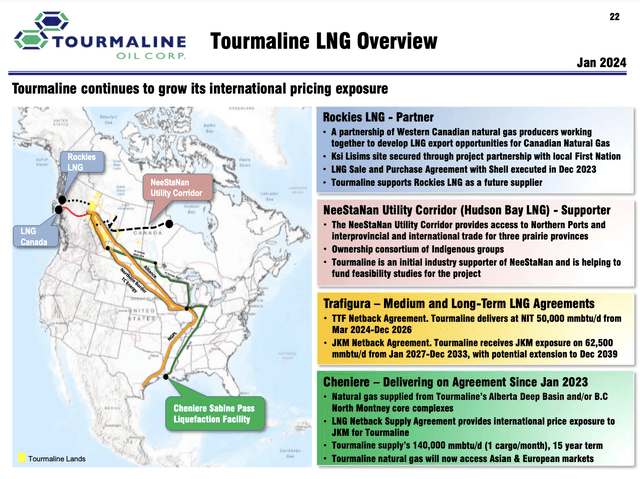

On top of that, the company is improving its pricing by engaging with new partners. This includes long-term liquified natural gas (“LNG”) deals with Cheniere Energy (LNG), Rockies LNG, and Trafigura.

Tourmaline Oil Corp.

All of this bodes very well for shareholders!

Special Dividends And A Great Valuation

I love special dividends, as special dividends are a great way to distribute excess cash without “committing” to consistent dividend growth.

Especially in the energy sector, which relies on volatile oil and gas prices, special dividends are a great way for companies to distribute cash.

While a good case can be made to prioritize buybacks over special dividends when energy equities are “cheap,” I like that Tourmaline has decided to opt for special dividends.

As we can see below, the company has used special dividends both consistently and aggressively in recent years. In 2022, it paid up to C$2.25 per quarter in special dividends. Using the current stock price, these numbers implied an annualized yield of 15%!

Tourmaline Oil Corp.

According to the company, it will grow its base dividend in line with production growth. As of 2Q24, the base dividend was C$0.33 per share, which translates to a yield of 2.2%. This dividend is breakeven at $1.50/Mcf

It also has declared a special dividend of C$0.50 every single quarter this year. This brings the total annualized yield to 5.6%, which is a fantastic number for a natural gas environment with prices consistently close to $2.

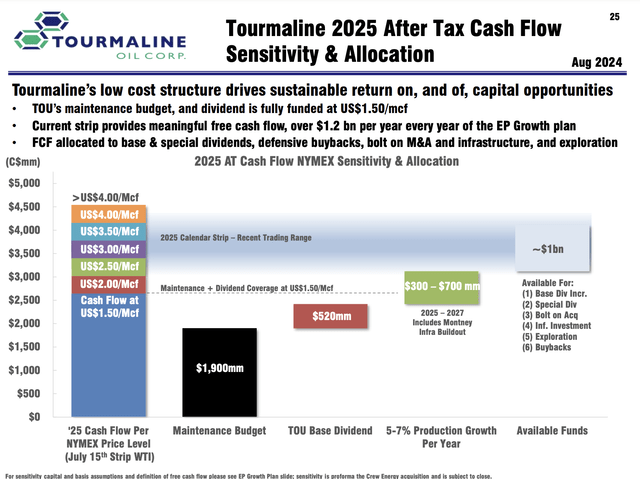

Moreover, to assess just how juicy this dividend can get, the company made the overview below. It spends roughly C$1.9 billion on maintenance and annual production growth costs up to C$700 million, including infrastructure output.

Assuming the natural gas bull case is correct, and we see $4.00 natural gas, the company could generate C$4.5 billion in operating cash flow. After maintenance and growth spending, we’re left with C$1.9 billion in free cash flow for the base dividend and special dividends.

This translates to 9% of its market cap. However, this assumes the upper bound of its growth CapEx range. The midpoint of that range pushes the implied free cash flow yield to 10%. Excluding growth CapEx, that number is north of 12%.

Tourmaline Oil Corp.

Needless to say, after 2027, the company’s production will be much higher and come with less hedging. This would significantly increase free cash flow potential, making TOU even more attractive.

As I expect higher natural gas prices than $4, I believe the company is significantly undervalued.

Other numbers confirm this.

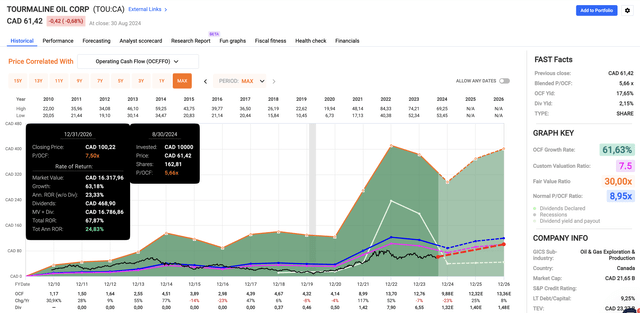

Using the FactSet data in the chart below, Tourmaline trades at a blended P/OCF (operating cash flow) ratio of just 5.7x. Applying the 7.5x multiple I have given other peers with similar qualities, we get a fair stock price of C$100, almost 70% above its current price.

FAST Graphs

This includes 35% expected cumulative per-share OCF growth in 2025 and 2026 – without incorporating a natural gas bull market(!).

Hence, on a longer-term basis, I expect TOU to move far beyond C$100, making it one of my top energy picks.

Takeaway

The current bear market in natural gas presents a significant opportunity for long-term investors.

Despite tough conditions, companies like Tourmaline Oil are in a great spot to thrive, thanks to their massive low-cost reserves, strategic acquisitions, and strong financials.

Tourmaline stands out with its attractive special dividends, growth potential, and a compelling valuation that suggests significant room for capital gains.

With the expected increase in natural gas demand and rising prices, I believe Tourmaline could deliver impressive returns, making it a top pick for anyone looking to capitalize on the future of natural gas.

Pros & Cons

Pros:

- Massive Reserves: Tourmaline has the largest low-cost natural gas reserves in North America, giving it a significant edge in a rising price environment.

- Special Dividends: I love their approach to rewarding shareholders with special dividends, offering a juicy yield without having to “commit” to unsustainable payouts.

- Strategic Growth: With the acquisition of Crew Energy and key partnerships for LNG exports, Tourmaline is in a fantastic spot to capitalize on increasing demand and higher prices.

- Attractive Valuation: The stock trades at a significant discount, with an upside potential that could push it far beyond C$100.

Cons:

- Volatile Natural Gas Prices: Natural gas prices are highly unpredictable and very volatile.

- Risk Exposure: The stock is not for conservative investors, as it has been through a lot of ups and downs. Despite my bullish outlook, it will remain as volatile as the commodities it produces.

- Sector Sentiment: Energy stocks, especially in natural gas, remain out of favor. It could take a few months until the bull case unfolds.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here