Lamb Weston Holdings (NYSE:LW) shares plunged on April 4, from just over $100 per share and were down about 20%, to the low $80 level. This was due to an earnings miss and reduced guidance. Overall, this appears to be an overreaction and for me, that means a potential buying opportunity. The earnings miss and reduced guidance seem to be (in large part) due to one-time issues. This is one reason why I see this as a buying opportunity, but there are other reasons which I will go into more below. A lot of investors may have never heard of this company, but almost everyone has consumed the potato products it makes, especially the French fries. Let’s take a closer look below:

As the data below shows, Lamb Weston has grown significantly over the past several years. This company was a spin-off from Conagra (CAG) in 2017, and that is why the financial comparisons started that year. Since 2017, revenues and profits have more than doubled. In addition, this company holds the #1 position in North America and #2 position globally for the frozen potato category. As a best-in-breed market leader, I believe it should be trading at a higher valuation than where it is today.

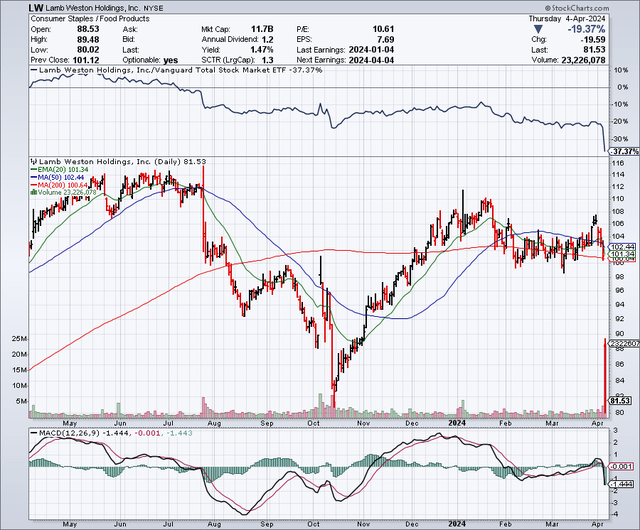

Lamb Weston Inc.

The Chart

As the chart below shows, Lamb Weston shares plunged from about $100, to just around $80 per share. It is notable to see that this stock had a similar plunge to the $80 level in October 2023, and within a few weeks the stock had rebounded back to the $100 level and later went even higher. This is encouraging for two reasons; one is the fact that this stock appears to have very strong support at the $80 level. If the stock holds this $80 level for a second time, this will create a very bullish double bottom on the chart. The other reason this is encouraging is because it shows this stock could have the potential to recover much if not all of what it just lost in this post-earnings plunge. Over the next few weeks, I would not be surprised to see this stock rebound back towards the 50-day moving average which is about $102 per share and the 200-day moving average which is around $100 per share.

StockCharts.com

The Earnings And Guidance That Caused The Plunge

Earnings for Q3 2024, were impacted by a couple of factors which were one-time issues. While these are disappointing, I don’t believe they merit a 20% plunge in the value of this company. Lamb Weston was impacted during this quarter by a transition to a new enterprise resource planning system and it also took a $25 million pre-tax charge to write-off excess raw potatoes. For Q3, the company reported non-GAAP earnings per share of $1.20 which missed by $0.25. Revenues came in at $1.46 billion, which missed estimates by $190 million. As for 2024 guidance, Lamb Weston expects to generate revenues of between $6.54 billion to $6.6 billion and it expects earnings to come in at $5.30 to $5.45 per share. The company explained the impact of the planning system impact by stating:

The transition to a new enterprise resource planning (ERP) system in North America negatively impacted our financial results in the quarter by more than we expected,” said Tom Werner, President and CEO. “The ERP transition temporarily reduced the visibility of finished goods inventories located at distribution centers, which affected our ability to fill customer orders. In turn, this pressured sales volume and margin performance. While we are disappointed with the magnitude of the ERP transition’s effect on the quarter, after implementing systems adjustments and modifying processes, we believe the impact is behind us as our order fulfillment rates have normalized.”

Analysts expect this company to grow in the coming years with earnings per share estimates of $6.59 for 2025, on revenues of $7.27 billion. For 2026, estimates are for $7.14 per share in earnings, on revenues of $7.69 billion. With these estimates, Lamb Weston shares are trading for just around 12 times forward earnings. This appears deeply undervalued when compared to many other food industry stocks and also when compared to the S&P 500 Index (SPY) which is trading for nearly 28 times earnings. In terms of the balance sheet, this company has about $3.63 billion in debt and around $78.3 million in cash.

The Dividend And Buybacks

Lamb Weston pays a quarterly dividend of $0.36 per share. This totals $1.44 per share annually and offers a yield of just under 2%. The next quarterly dividend will be paid on May 31, 2024, to shareholders of record on May 3. Lamb Weston has a history of dividend growth. Back in 2017, the quarterly dividend was $0.1875 per share, but it has just about doubled over the past 8 years, thanks to consistent increases.

For the first three quarters of 2024, this company repurchased $150 million in shares and there was $450 million remaining under the current share buyback plan. With the shares down significantly after the Q3 earnings report, I would hope that the company will soon put some of the remaining share buyback funds to use.

What I Like About Lamb Weston

This company is a market leader that has grown significantly over the past few years. It is also a dividend growth stock that could continue to see future increases in the payout. This company sells to grocery stores and it also sells to many of the largest quick service restaurants in the industry. Food in general is a relatively recession resistant business and that is another positive. The share buyback is another aspect that could help support the stock and increase future earnings. I am also a happy consumer of Lamb Weston French fries, which are a regular staple in my freezer.

Potential Downside Risks

Management execution is a potential downside risk, in particular since the transition to the new planning system did not seem to go as expected. A recession could cause a mild slowdown, but I see this as a small risk since fries and potatoes and fast food restaurants tend to remain strong during downturns. Supply chain and geopolitical issues could be a potential downside risk as well, since this company operates globally.

In Summary

This 20% plunge appears to be an overreaction, especially since the earnings and guidance miss appear to have been caused by one-time issues. This stock rebounded quickly during the plunge it had in October, and it once again seems to be finding strong support at around the $80 level. I feel this is an ideal buying opportunity for a stock that is an industry leader and the valuation is cheap at just around 12 times forward earnings. I believe this stock can rebound in the next few weeks and I plan to add more shares on any further weakness.

Read the full article here